%20RISE%20Rulemaking%20Final%20.avif)

The U.S. Department of Education’s Reimagining and Improving Student Education (RISE) committee completed its second negotiated rulemaking session in November 2025—bringing some of the biggest student loan policy changes in more than a decade.

These new rules reshape how borrowers repay their loans, the repayment plans available, how much students and parents can borrow, and how schools structure financial aid.

This SEO-optimized guide breaks down the final RISE Rulemaking decisions, explains what changes take effect in 2026, 2027, and 2028, and helps borrowers understand how these updates will impact their student loans.

Key Takeaways

- PAYE, SAVE, and ICR end by 2028, while RAP becomes the new IDR plan in 2026; IBR stays only for existing borrowers who avoid new loans or consolidation.

- Graduate PLUS Loans and Parent PLUS Loans face major caps starting 2026, including new annual and lifetime borrowing limits for parents, graduate students, and professional students.

- A new $257,500 lifetime federal loan limit takes effect July 2026 for most federal loans.

- Default relief options shrink in 2027, including limits on rehabilitation, removal of unemployment/economic hardship deferments, and stricter forbearance caps.

- Schools may set lower borrowing limits for specific academic programs starting in 2026.

1. New Rules for Student Loan Rehabilitation (Starting July 2027)

Many borrowers search for help with how to get out of student loan default. Under the new RISE regulations:

✔ Only Two Loan Rehabilitations Allowed (After July 1, 2027)

Borrowers can rehabilitate a defaulted federal student loan only twice in their lifetime.

✔ One Wage Garnishment Suspension Per Rehabilitation Attempt

Borrowers seeking to pause administrative wage garnishment through rehabilitation will only get one suspension per attempt.

2. Major IDR Plans Eliminated by 2028 (PAYE, SAVE, and ICR)

Borrowers researching which income-driven repayment plans are ending will see major changes:

Plans Ending for All Borrowers

- PAYE (Pay As You Earn)

- SAVE (Saving on a Valuable Education)

- ICR (Income-Contingent Repayment)

Timeline:

- No new enrollments after July 2026

- Fully discontinued by July 2028

These eliminations reduce the number of income-driven repayment plans from several options down to only two: IBR for existing borrowers and RAP for new ones.

3. IBR Will Remain for Current Borrowers

If you’re asking “Will IBR still be available?”—the answer is yes, with limitations.

Borrowers can stay enrolled in IBR if they:

- Do not consolidate after July 2026

- Do not take out new federal loans after July 2026

IBR continues to offer 20- or 25-year student loan forgiveness depending on your original loan date.

However, borrowers switching out of IBR may experience interest capitalization, which increases the balance.

4. RAP Becomes the New Standard Income-Driven Repayment Plan

Beginning July 2026, the Repayment Assistance Plan (RAP) will replace all other IDR options for new borrowers. RAP will be the default for anyone starting college or graduate school after that point.

Key Features of RAP

- Income-based payments, but no income protection, meaning all borrowers—regardless of income—must pay something.

- 30-year forgiveness, longer than IBR.

- Interest subsidies help reduce ballooning balances.

- Higher payments for most borrowers compared to SAVE or PAYE.

Borrowers can switch between IBR and RAP, but consolidating after July 2026 removes IBR eligibility forever.

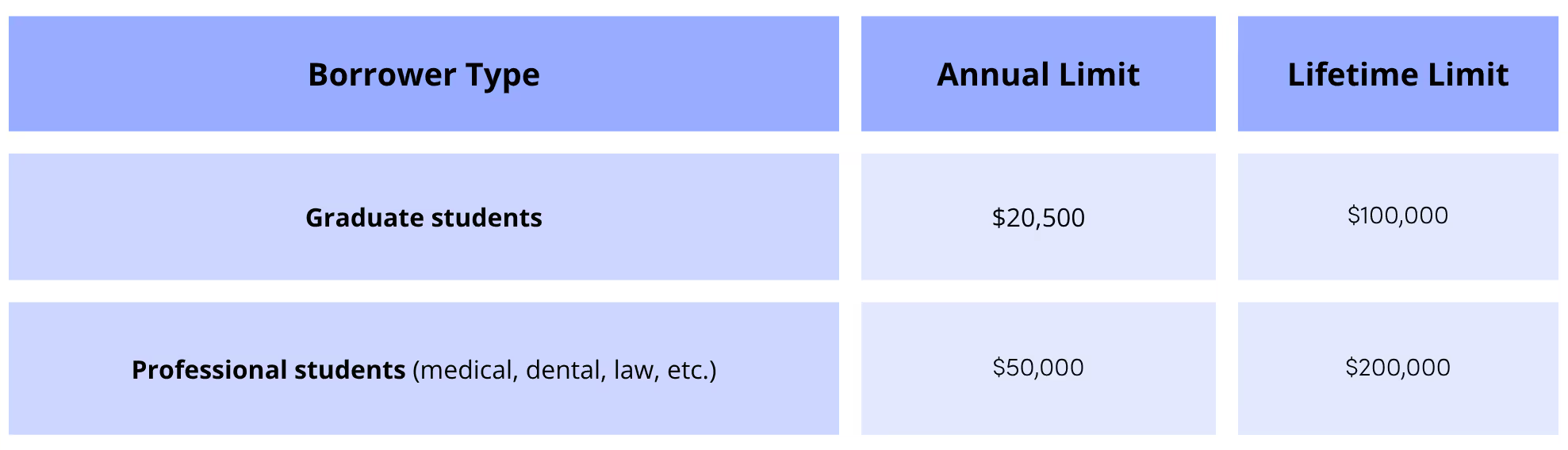

5. Big Changes for Graduate and Professional Student Loans

Many graduate borrowers search for “Are Graduate PLUS Loans going away?” Yes—they are.

✔ Graduate PLUS Loans Eliminated After July 1, 2026

New Borrowing Caps (Effective 2026)

Students enrolled before July 1, 2026 may continue borrowing at old limits only for their current program.

Purpose of the new rules:

To reduce excessive graduate school borrowing, slow tuition inflation, and encourage cost transparency.

6. Parent PLUS Loans Will Also Be Capped

Currently, Parent PLUS Loans allow borrowing up to the full cost of attendance. Under the RISE final rules:

✔ New Parent PLUS Loan Caps (Starting 2026)

- $20,000 per year per child

- $65,000 lifetime limit

Parents seeking IDR for Parent PLUS loans will need to consolidate before July 2026 to preserve access.

7. New Lifetime Federal Student Loan Limit: $257,500

Beginning July 1, 2026, the federal government is setting a lifetime borrowing cap, excluding PLUS loans:

✔ Lifetime Maximum: $257,500

This applies across all undergraduate and graduate loans (again, not including Parent PLUS or Grad PLUS prior to elimination).

Students enrolled before July 2026 can exceed this amount only if they remain in the same program.

8. Deferment and Forbearance Options Will Shrink

Borrowers often search for “student loan deferment and forbearance rules,” and these are changing significantly.

Unemployment Deferment

- Allowed only for loans disbursed before July 1, 2027

- Eliminated for loans disbursed after July 1, 2027

Economic Hardship Deferment

- Same rule as above—ending for new loans after July 2027

General Forbearance

- For new loans disbursed after July 2027:

Maximum of nine months within any 24-month period

Borrowers will need sustainable repayment support rather than long deferment periods.

9. Reduced Borrowing for Less-Than-Full-Time Students (Starting 2026)

Loan amounts will be prorated based on the percentage of full-time enrollment. This affects borrowers searching for “Can part-time students get federal loans?” and aligns borrowing with actual course load.

10. Colleges Can Set Their Own Lower Loan Limits

Starting July 2026, institutions may reduce borrowing limits for specific academic programs—especially those with lower expected earnings—if:

- Limits apply equally to all students in that program

- Students receive clear, advance notification

This is intended to prevent over-borrowing in low-wage career paths.

What Borrowers Should Do Before These Changes Take Effect

✔ If you want to stay in IBR

Avoid consolidating and avoid new loans after July 2026.

✔ If you’re a parent borrower

Consolidate before July 2026 to keep IDR eligibility.

✔ If you're a graduate or professional student

Confirm whether you're “grandfathered” into current borrowing rules.

✔ If you’re in PAYE, SAVE, or ICR

Expect to be transitioned into IBR or RAP.

✔ If you're at risk of default

Talk to a student loan advisor early—rehabilitation opportunities will soon be limited.

The final RISE rulemaking decisions bring some of the most significant changes to federal student loans in years—limiting repayment options, redefining borrowing limits, and shifting how both students and parents plan for higher education. Whether you’re navigating the transition away from PAYE or SAVE, preparing for RAP, or reassessing graduate or Parent PLUS borrowing, these updates can feel overwhelming. Remember: you don’t have to figure this out alone. Understanding these new rules is the first step toward choosing the right repayment path, protecting your financial future, and staying on track for forgiveness programs like PSLF. As these regulations roll out from 2026 to 2028, staying informed—and getting expert guidance—will be essential for making confident, well-planned decisions about your student loans. If you’re unsure how these changes affect you, reach out for support so you can move forward with clarity and peace of mind.